Price Discovery for Dedicated Blockspace

Part 2: Understanding Saga's Token Economics

Introduction

In our previous blog post, we analogized Saga’s core technology to Amazon Web Services: As AWS made hosting web applications easier for Web2 companies, Saga aspires to do the same for blockchains and Web3 projects. In this post, we’ll dive into the details of the economic model that powers Saga’s core product: The automated instantiation and orchestration of blockchains. Similar to cloud computing, Saga’s core product can be likened to a commodity. We’ll start by giving a broad overview of the marketplace dynamics for a traditional commodity like gold and contrast that to the marketplace for validation services in Web3. Then, we’ll discuss how Saga’s economic design solves a key problem that is inherent in the validation services marketplace. Finally, we’ll discuss some of the key economic mechanisms that will be implemented into the Saga protocol that will lead to long-term downward pressure on the price of validation services. Let’s dive in.

Price Discovery for Traditional Assets

Price discovery for assets or commodities is typically determined via the interaction of buyers and sellers in a marketplace. In the case of traditional commodities, such as agricultural products or precious metals, this process will usually involve buyers and sellers coming together to negotiate and agree on a price. Traditionally, this has been facilitated via open outcry, where buyers and sellers shout out their bids and offers to each other. More recently, buyers and sellers can place orders and trade with each other in real time via electronic trading platforms.

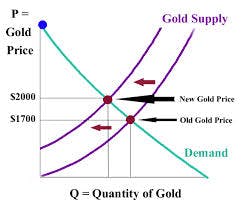

Consider a commodity like gold. The marketplace for buying and selling gold can include gold-mining companies, investors who buy and trade gold as a store-of-value, speculators, central banks, jewelry manufacturers, companies that utilize gold in industrial applications and any individuals that may want to buy or sell gold for personal use. Gold can be exchanged in multiple venues, from jewelry stores and pawn shops to global exchanges, where individuals can buy and trade at current prices today and speculate on the gold price in the future. Large exchanges like Chicago Mercantile Exchange and Shanghai Gold Exchange and smaller entities all function together to create an open marketplace for gold. We define an open marketplace as a marketplace where any number of buyers and sellers can come together to negotiate prices and exchange value, and there are few restrictions put in place on who can buy and sell. In an open marketplace, the value of a commodity like gold is simply a function of supply and demand. If the demand for gold at a particular moment rises while supply remains constant, the price of gold will go up. Similarly, if the supply of gold on the market increases while demand remains constant, the price of gold will go down.

Price Discovery for Validation Services

The marketplace for validation services for Web3 blockchain networks has a supply and demand component. On the demand side of things, there are many proof-of-stake networks that require validator services. The Solana network has nearly 2,000 validators, Ethereum boasts over 400,000 validators, and there are dozens of other networks like Polkadot and Juno that each require 100+ validators to operate their chain. On the supply side, there are many entities that can offer validation services. For example, a company like Strangelove offers validation services to multiple networks like Cosmos Hub, Akash and Osmosis. Other entities like Lido can create multiple validators for a single network like Ethereum. It’s difficult to determine the number of entities in Web3 that offer validation services because of their decentralized and sometimes anonymous nature, but safe to say there are likely thousands of such entities that exist today.

The marketplace for validation services in Web3 resembles an open marketplace in the sense that there are few restrictions on who can launch a blockchain network and who can offer validation services. That said, the marketplace for validation services for each network is distinct. Whereas the gold market is homogenous (the gold that is traded on the Chicago Mercantile Exchange is identical to the gold that is traded on the Shanghai Gold Exchange), the value exchange for validation services on one network is fundamentally different from other networks.

For example, on the Solana network, validators are required to run a machine with at least 2.8 GHz, 128GB RAM, 1TB of storage, a fast internet connection and are paid in $SOL tokens for their service. For Ethereum, the machine requirements are lower and validators are paid in $ETH. Because the price of $SOL and $ETH is known, and both tokens have deep liquidity, a validator can reasonably assess the revenue that can be brought in by offering validation services and weigh this against the costs to determine whether profitability is possible.

For new networks, it is much more difficult to assess potential profitability. Because validators are typically paid in network tokens (like $ETH and $SOL), validators for new networks get paid in new minted network tokens. New network tokens often have limited liquidity and exhibit extreme price volatility, even by crypto standards. The number of users for new networks is typically small, which makes it difficult to assess total network value. Founders of new networks often have to resort to actively recruiting or even bribing validators in some manner to compensate them for the uncertainty that surrounds offering validation services; this is not ideal for the functioning of a proper marketplace. The Saga protocol addresses this issue by specifying the price for validation services for new chains. To understand how this price is determined, let’s dive into Saga’s economic design.

Saga’s Economic Design

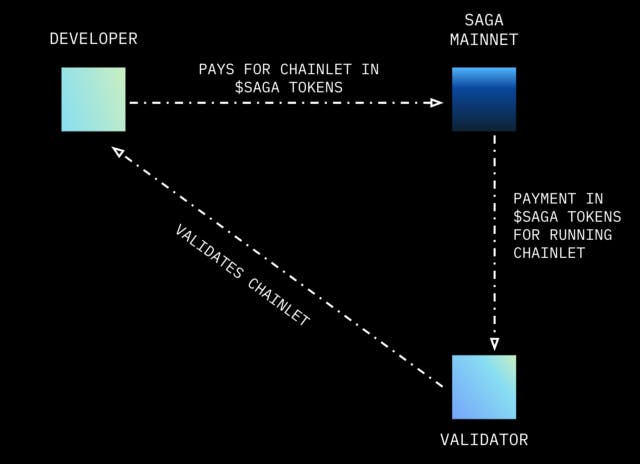

Saga’s core product solves problems for both validators and teams that want to create a new blockchain network by determining an exact price of validation services. The mechanisms put in place also lead to price stability over time. When the price of validation services is known ahead of validation, validators can more accurately determine the profit or loss that they may accrue. By determining the price of validation services ahead of time, teams no longer need to recruit or bribe validators; rather, they need to determine whether they can afford the predetermined cost that must be paid. The price for validation services is quoted in $SAGA tokens, and the blockchains that are run via the $SAGA payments are known as chainlets.

It’s important to note that the validators who already provide validation services for the Saga network are eligible to receive $SAGA tokens for validating chainlets. In proof-of-stake blockchain networks, there is always a limited number of validators who have the privilege of running a validator. A limited number of validators per network ensures that the network can reach consensus within a certain amount of time. A typical Cosmos chain will have anywhere from 75–100 validators, with some networks such as Crescent with as few as 50 active validators and other networks such as the Cosmos Hub with as many as 175 validators. Given the limited number of slots for validators, the price for offering validation services does not follow the normal rules of supply and demand of an open marketplace.

Validator Groupings

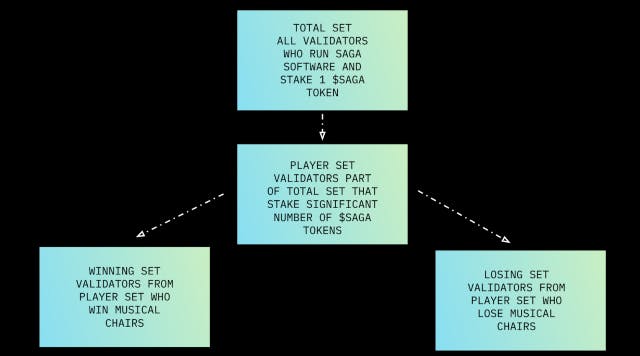

So what determines the price of validation services? Before answering this question, we must first understand the different validator groups for the Saga network. From the large pool of entities that offer validation services in Web3, any number of those entities can signal a desire to validate Saga chainlets by doing two things: first, create a new validator that runs the Saga software, and, second, acquire and stake a negligible amount of $SAGA token. By staking $SAGA tokens, a validator shows that they are willing to put financial capital at risk in order to join the network. This locked financial capital serves as a basis for determining the size of the financial incentive or punishment that is tied to the quality of the validation services that is provided. By staking $SAGA token, a validator can be included in what we define as the “total set” — the set of all validators who run the Saga software and have financial risk at stake via locking up $SAGA tokens.

From the “total set” of validators, a validator can be included into a more exclusive club known as the “player set”. The distinction between the player set and the total set is that validators in the player set have staked a significant number of $SAGA tokens (the specific number is determined by the stake distribution), which represents a more serious financial commitment. The player set can be divided into a “winning set” and a “losing set”. The validators in the winning set are the validators who validate the Saga network and are eligible to validate chainlets in exchange for $SAGA tokens; the validators in the losing set are not eligible to validate chainlets. Validators are grouped into the winning set or losing set based on their actions in an auction mechanism known as musical chairs.

Musical Chairs

Musical chairs is a game that many children have played. It involves a group of players who walk in a circle around a number of chairs while music is playing. When the music stops, the players must scramble to sit down in one of the chairs. However, there is always one fewer chair than the number of players, so one player is left standing. The player who is left standing is eliminated.

The Saga auction mechanism is similar to musical chairs. Validators in the player set have an opportunity to declare the price (in terms of $SAGA tokens) that they are willing to accept to validate chainlets. Once these prices are declared, validators are then ranked according to their price offering — the lower the price, the better their ranking. The validators that are determined to be part of the winning set are the ones who offer the lowest price for validation services. The remaining validators that declared a price higher than their competitors will find themselves without a chair and end up as a part of the losing set. The price for validating Saga chainlets is then set at the highest price that is found in the winning set.

For example, let’s say there are 12 validators who are part of the “total set” — they run the Saga software and have locked a small amount of $SAGA. Of these 12 validators, only 10 of these validators meet the requirements for having staked a significant number of $SAGA tokens to be included in the “player set”. These 10 validators then declare their price for offering validation services as the first step of the musical chairs auction. Only 8 validators can be included as part of the Saga network, which means that only 8 validators can be a part of the winning set. The 10 validators are then ranked according to their declared price. The validators who declared any of the lowest 8 prices for their services will be a part of the “winning set”. The remaining 2 validators are then included as part of the “losing set,” and the price for validating chainlets is set at the highest price that was declared by any of the winning set validators. This ensures that every validator in the winning set will validate chainlets at a price greater than or equal to the price than they bid during the auction process.

The price of validation services for Saga chainlets is not static. The musical chairs auction is a repetitive event, which makes the price of validation services a dynamic variable that can change over time.

Price Discovery for Saga Chainlets

So how do the validator groupings and the musical chairs auction mechanism impact price discovery for validation services? If validators that are a part of the player set bid too high during musical chairs, they risk being relegated to the losing set and missing out on a potential profit opportunity. On the other hand, if a significant number of validators bid too low, they risk running their validation services business at a loss, as the revenue generated from validating chainlets may not cover their costs. As a result, validators are encouraged to declare a price that will allow them to run at a small profit; this maximizes the chance of being able to run a profitable business validating Saga chainlets. Validator groupings and musical chairs also encourage validators to optimize their business operations over time so that they better their chances to continue running profitable validation services for Saga. Put another way, validators who run an efficient business will have a high likelihood of being in the winning set and creating profits in the short-run. Validators who continue to optimize their business to run more efficiently over time will have a high likelihood to stay in the winning set in the long-run.

Price discovery for validation services in Saga’s ecosystem differs from an open marketplace like gold in one key manner: only a limited number of entities can offer validation services. In contrast, just about anyone in the world who has gold has the opportunity to sell it. Because there is a limited number of slots available, we can implement a mechanism whereby the protocol chooses validators that offer the cheapest service and also have a significant financial stake at risk. Such a mechanism could not be implemented in an open marketplace.

Price discovery for validation services in Saga’s ecosystem differs from validation services for new networks in a key manner: the price for validation services is known ahead of time for both validators and network founders. This enables the functioning of a robust marketplace free of validator recruitment without the necessity for bribes. Currently, there is no robust marketplace for validation services in Web3. Saga will create the first such marketplace.

What Does this Mean for Saga Developers?

So what does this all mean for teams that want to deploy their own blockchain on Saga? The mechanisms described above ensure that the price for validation services stays relatively close to the actual cost to offer validation services. While this is a nice property of our token economic model, there are many unanswered questions. How much money does it actually cost for teams deploying chainlets on Saga? How much variability could there be in blockchain pricing over time? What economic models can developers deploy to make money from their blockchain? To answer these questions, we’ll need to understand a few new ideas: fee deposits, the scheduler function, TWAP blockspace pricing, and flexible gas fees. We’ll dive into these ideas in part 3 of this series.